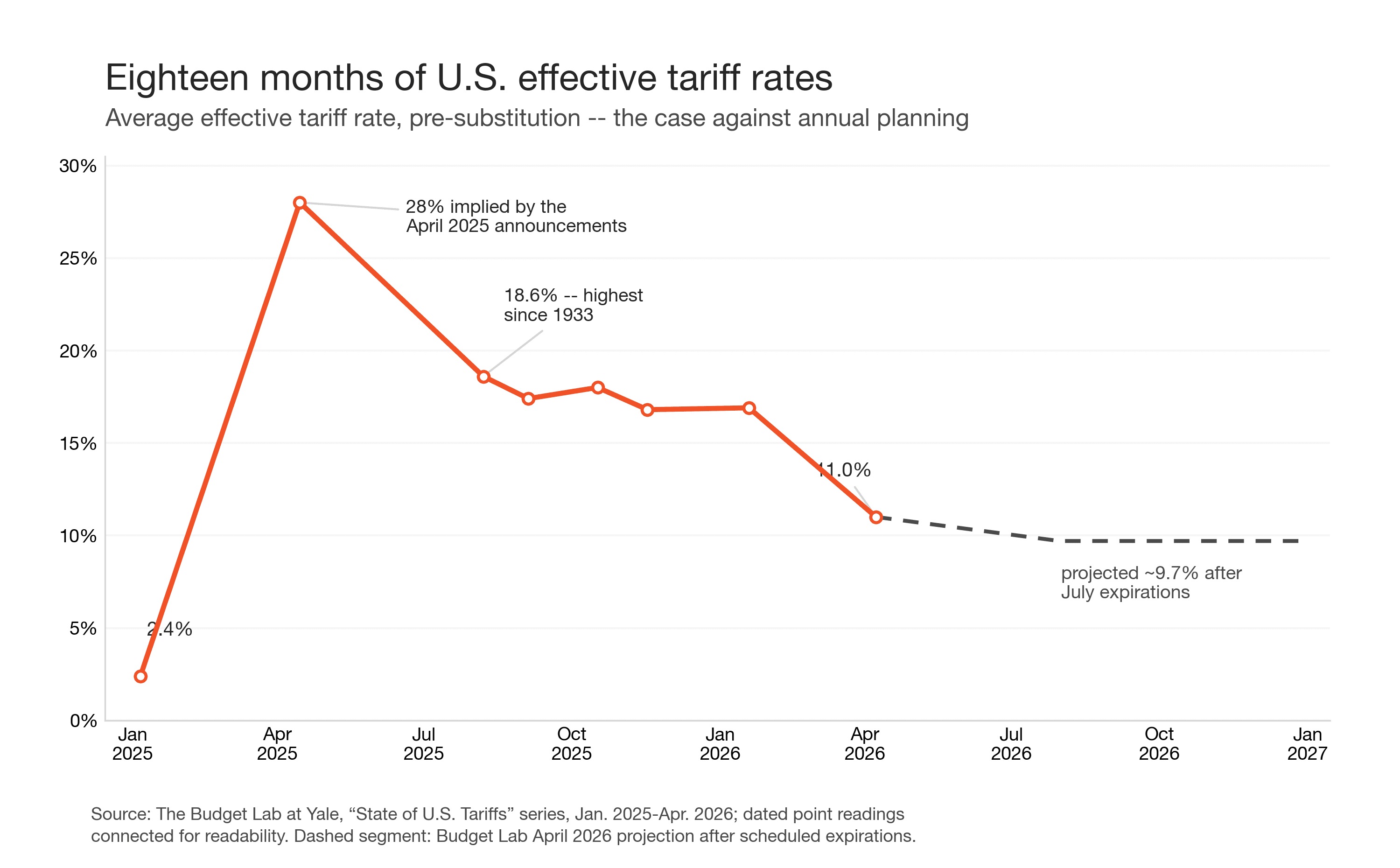

Follow one number through the last eighteen months. The average effective U.S. tariff rate started 2025 at 2.4%. The announcements of April 2025 briefly implied a rate near 28%. By August the dust had settled at 18.6% -- the highest level since 1933 -- and then the exemptions and deals began: 17.4% in September, 18.0% in October, 16.9% in January. By this April the rate stood at 11.0%, and The Budget Lab at Yale projects roughly 9.7% once the Section 122 tariffs expire in July and the pharmaceutical tariffs arrive in September.

Related: the feed-forward idea this playbook leans on is part of a bigger argument -- Closed-Loop Procurement.

That is four distinct trade regimes inside eighteen months, spanning exactly one annual budget cycle. If your landed-cost assumptions were set in January 2025 and reconciled in December, the number you planned against was wrong by a factor of seven at the peak, and wrong in both directions before the year closed.

Most of what procurement people read about tariffs is written by trade lawyers and freight forwarders, and it shows: the advice is about entry filings and shipping lanes. This post is the buyer's version. Duty is now a cost element that moves faster than most commodity indices, and the levers that actually manage it -- classification, origin, valuation, recovery, negotiation -- are sourcing levers. They belong to whoever owns the bill of materials.

The number that would not sit still

It is worth sitting with the volatility for a moment, because it changes what kind of problem this is.

A stable tariff regime is a compliance problem: classify correctly, file correctly, audit occasionally. The 2025-2026 regime is a sourcing problem. When the rate on a Chinese subassembly can triple between quote and first shipment, and then fall by a third before the tooling amortizes, tariff exposure behaves like a volatile commodity input -- except that, unlike copper or resin, it moves on signatures rather than supply and demand, which means it gaps overnight and ignores your hedges.

Point readings from The Budget Lab's dated reports, connected for readability; the dashed segment is their April 2026 projection.

The buyers I watch getting through this are not the ones forecasting rates better. Nobody forecasts this well -- the Budget Lab's own reports read like weather bulletins. The buyers doing fine are the ones whose cost models absorb a rate change the way a good ERP absorbs a price change: as a data update, not a crisis meeting.

Duty is a BOM line, not a freight surcharge

Here is the structural problem with how most companies account for tariffs: they land in a freight or landed-cost bucket, blended across a category, visible only in aggregate. A surcharge arrives after every decision is frozen -- the part designed, the supplier quoted, the origin set, the contract signed. By the time duty shows up as a number anyone reviews, the choices that created it are months old.

A BOM line is different. It sits where the choices still exist.

The single highest-value change a procurement team can make on tariffs is accounting hygiene: carry duty as its own line on every exposed part -- HTS code times country of origin times customs value. A die casting from Vietnam, a wire harness from Mexico, and a machined bracket from China can sit in the same assembly with entirely different duty exposure and entirely different escape routes. Blend them and you can see that margin moved; you cannot see why, or what to do about it. Line them out and duty becomes what every other BOM element already is: should-costable, quotable, negotiable, and trackable against alternatives. It is the difference between knowing your total landed cost as a fact and knowing it as an average.

It also becomes forecastable, which matters more than usual right now. Announced-but-not-yet-effective changes are free information: the July expirations and September pharmaceutical tariffs are published, not speculative. A control engineer would call pricing them in before they hit feed-forward; a buyer should just call it Tuesday. Quote exposed parts three ways -- at award-date rates, at start-of-production rates, and at announced future rates -- and let finance reserve against the gap while sourcing works the mitigation list.

One clarification on ownership, because this is where the org chart usually fumbles the handoff. Trade compliance owns the legal entry, and nothing here changes that. But by the time an entry exists, most of the decisions that created the exposure -- supplier, location, value chain, contract terms -- were made at a sourcing desk, usually months earlier. Duty math has to live where those choices are made, with compliance as the control authority, not the discovery mechanism.

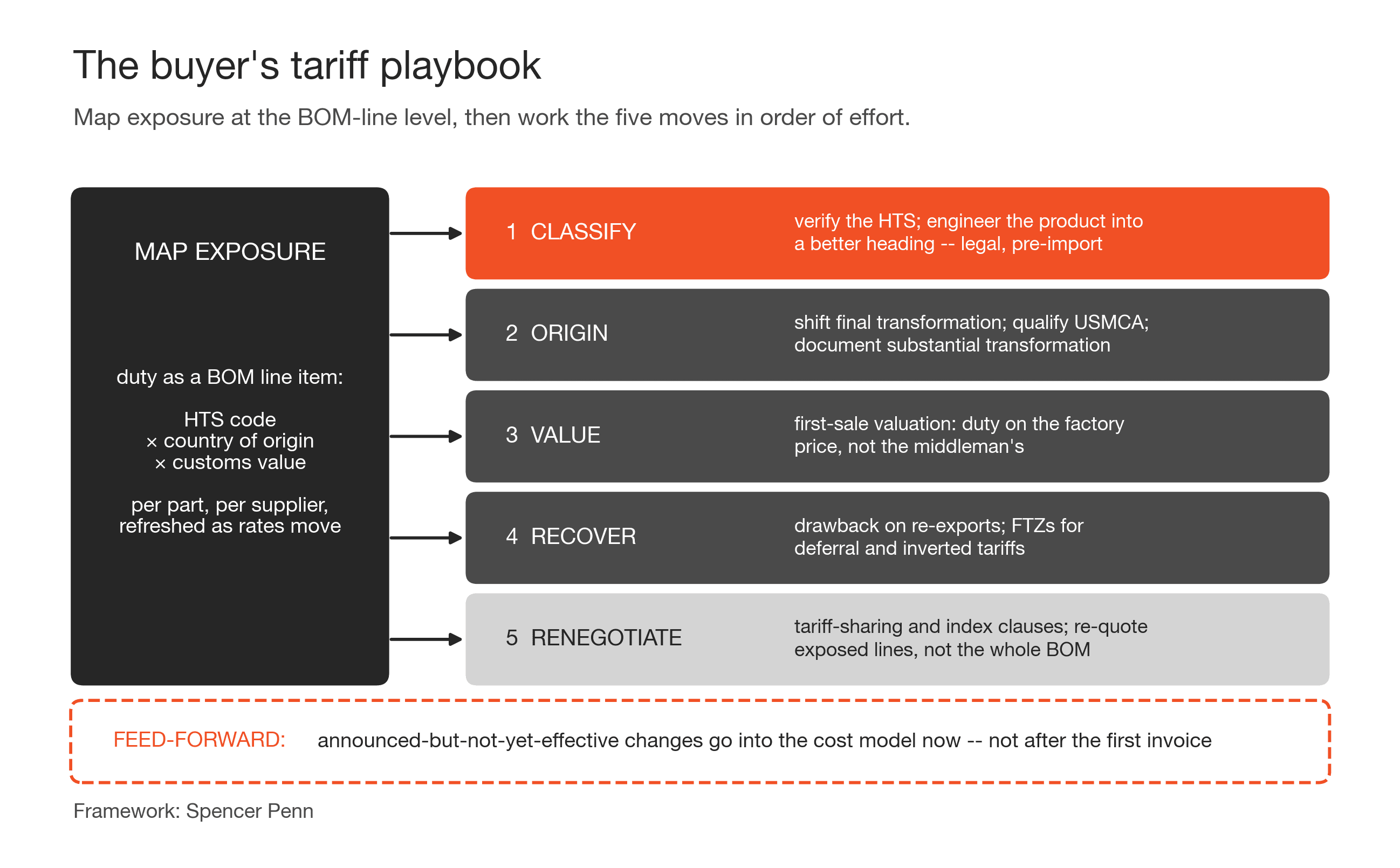

Move 1: Classify -- and engineer

Start with the unglamorous step: confirm that every exposed part's HTS code is actually correct. The Harmonized Tariff Schedule runs to ninety-nine chapters and the classification logic is genuinely tricky at the margins; misclassification cuts both ways, and overpaying is just as common as underpaying. On a BOM of any size, a classification audit of the top duty-paying lines is the fastest money in this post.

Then look for engineering options, because classification follows the physical product as imported -- and companies have been legally designing their way into better headings for over a century. The classics are worth knowing because they calibrate what counts as real:

Converse ships All Stars with a thin layer of felt on the outsole. Footwear with felt-covered soles classifies differently than athletic shoes, at a fraction of the duty. The felt wears off in weeks; classification is assessed at the moment of import, so the duty savings do not.

Columbia Sportswear adds small pockets below the waistline on certain women's shirts, moving them out of a 26.9% blouse classification into a 16% category. A designer, a customs broker, and a margin target, all in one garment.

The Snuggie's maker went to court over whether a fleece robe with sleeves is a garment or a blanket, and in 2017 the Court of International Trade ruled it a blanket -- 8.5% duty instead of 14.9%.

The pattern in all three: a real, physical, pre-importation product attribute, honestly declared, that genuinely changes what the thing is under the tariff schedule. For a manufacturer, the equivalent conversations are about material substitutions, where a subassembly gets joined, and what state of completion a part ships in. Those are engineering change orders with duty consequences -- run them through the same should-cost discipline as any other design-to-cost decision, and get a binding ruling from CBP when the classification is aggressive. A ruling letter is cheap; the alternative section of this post is not.

Move 2: Origin

Duty follows where the last substantial transformation happened, not where the purchase order went or where the supplier's headquarters sits. That makes origin a designable property of your supply chain -- within real limits.

Substantial transformation means the product genuinely became a different article of commerce somewhere: new name, new character, new use. Moving final processing steps, qualifying parts under USMCA content rules, and documenting the transformation properly are sourcing decisions a buyer controls, and in a high-tariff regime they deserve the same rigor as a make-versus-buy or dual-sourcing analysis. The China-plus-one conversations most manufacturers have been having for years are, among other things, origin-engineering conversations -- and the same compliance care applies to them as to China's own tightening export rules.

The caution is structural: paper routing is not origin engineering. A Chinese part that takes a boat detour through a third country and picks up a new label is still Chinese under the law, no matter what the certificate says. More on what happens to that move below.

Move 3: Value

Duty is a percentage of customs value, which makes the valuation basis the quietest lever on this list. The first-sale rule lets qualifying importers declare value based on the first sale in a multi-tier transaction -- the manufacturer's price to the trading company or intermediary -- rather than the marked-up price the importer actually pays.

On a part with a 25% duty and a 15% intermediary markup, first-sale valuation claws back nearly four points of landed cost without changing the product, the supplier, or the logistics. The requirements are strict: a bona fide arm's-length first sale, goods clearly destined for the United States at the time of that sale, and documentation that proves both -- purchase orders, invoices, payment records, and any assists accounted for. That paperwork burden is exactly why adoption stays low, and why the importers who build the documentation muscle keep the savings year after year. It is a classic cost-avoidance program: invisible in a savings report, very visible in landed cost.

Move 4: Recover

Money already paid is not necessarily money gone. Duty drawback refunds up to 99% of duties, taxes, and fees on imported goods that are subsequently exported or destroyed -- including substitution drawback, which matches imports and exports at the HTS level rather than requiring you to trace the physical molecules. Import components, build product, export some of it, and a meaningful slice of your duty bill is refundable.

The scale of the unclaimed pool is striking. CBP pays out roughly $1 billion a year in drawback, per the Government Accountability Office -- and industry estimates put the eligible refunds left unclaimed at several times that, mostly because the documentation feels daunting and nobody owns the program. The mechanics deserve their own post, and they have one: our practical guide to duty drawback walks through eligibility, filing, and the records you need. The strategic point belongs here: drawback fails when it is treated as an accounting cleanup. If export links, serial numbers, and entry data are not tagged at award time, the refund becomes archaeology. Design recovery into the sourcing data from day one.

Foreign-trade zones round out the recovery lane: duty deferral until goods leave the zone, no duty at all on re-exports, and -- in inverted-tariff cases where components carry higher rates than finished goods -- a structural rate reduction for manufacturing inside the zone.

Move 5: Renegotiate

Now the move most buyers reach for first, armed with the data to do it properly.

The New York Fed's analysis of who actually paid the 2025 tariffs found that about 90% of the burden landed on U.S. firms and consumers -- foreign exporters did not, in aggregate, eat much of it. But the average hides the finding that matters for a buyer: at the level of established importer-exporter relationships, pass-through ran 65-70%, and large buyers with bargaining power paid measurably less than small ones. Who absorbs the duty is a negotiation, not a law of nature, and passivity means paying the sticker rate.

Bargaining power is not personality. It is qualified alternatives, clean cost models, and credible volume movement -- the same assets that win any negotiation, pointed at a new cost element. Re-quote the exposed BOM lines specifically rather than asking for blanket relief; a supplier who sees you know exactly which parts carry which duty at which origin negotiates differently than one fielding a vague request to share the pain. Watch for price variance that quietly exceeds the actual statutory change -- tariff noise is a popular place to hide margin expansion, in both directions.

Then write the clause properly, because the 2025-2026 whipsaw taught everyone that rates fall too. A complete tariff clause defines the baseline HTS code and origin, the duty rate at signing, the valuation method, proof requirements, the sharing mechanism, a cap, a sunset, and a reopener -- so that when the rate drops, the price comes down by the same logic that raised it. Buyers who wrote one-directional clauses in 2025 are re-learning this now, on the wrong side of an 18.6%-to-11% move.

Smaller importers without volume to wield can still run most of this play: isolate the exposed lines, aggregate demand across plants and business units, prequalify a second source at a different origin as negotiating infrastructure, and refuse blended price increases that bundle duty with everything else.

The line between engineering and evasion

Everything above is legal, established, and in several cases blessed by federal courts. Its mirror image is a federal felony, and 2026 is the wrong year to confuse them.

The enforcement climate is the harshest in decades. The Justice Department stood up a dedicated Trade Fraud Task Force in August 2025, pairing DOJ attorneys with CBP's Office of Trade and Homeland Security Investigations. CBP issued 1,400 trade-enforcement penalties in the first half of 2025, on pace to beat every year in recent memory. False Claims Act recoveries hit an all-time record of $6.8 billion in fiscal 2025, with 1,297 whistleblower suits filed -- also a record. And four weeks ago, the task force announced the largest customs-fraud settlement in U.S. history: $549.5 million against an importer that evaded antidumping duties on Chinese aluminum. Another recent settlement involved Chinese tungsten carbide routed through Taiwan with relabeled origin paperwork.

The distinction between the playbook and the docket is not subtle. Felt on a sole is a real product, honestly declared, classified accordingly: engineering. A Taiwanese label on a Chinese part is paperwork pretending to be a supply chain: fraud. What has changed is the detection. CBP now runs AI-driven supply-chain analytics against import patterns to flag transshipment and undervaluation, and the False Claims Act pays whistleblowers a share of recoveries -- and the people best positioned to blow the whistle are your own employees, your competitors, and your suppliers.

The operating standard that follows: make the file readable by someone hostile. Every change in classification, origin, valuation, or recovery treatment should show what physically changed, who approved it, what documents support it, and which counsel or broker reviewed it. Binding rulings, origin documentation, first-sale paper trails -- the compliance file is not overhead on the playbook. It is the playbook's license to operate.

Where the desk work goes next

The reason most teams have not done what this post describes is not that any single move is hard. It is that the data work underneath -- duty at the BOM line, per part, per origin, refreshed as rates move, wired into quoting -- has historically been brutal to maintain by hand in spreadsheets. That is changing. Our customers at LightSource -- mostly challenger manufacturers running fast NPI cycles -- track tariff exposure at the BOM line, run what-if scenarios when an origin shift or rate change is announced, and re-quote the exposed parts in hours rather than quarters. The duty column updates the way the rest of their cost model does: continuously, not at budget season.

The rate will move again -- July's expirations, September's pharmaceutical tariffs, an election cycle behind those. The lesson of the last eighteen months is not which direction comes next; it is that nobody reliably knows, and the annual cost-down ritual was never built for a cost element that gaps overnight on a signature. The buyers getting through this are not forecasting better. They carry duty math in the BOM, they have rehearsed five legal moves, and when the schedule changes, they re-quote a column instead of convening a task force.

Sources

The Budget Lab at Yale: State of U.S. Tariffs, April 8, 2026 -- effective rate 11.0%; projections after July expirations and September pharmaceutical tariffs

The Budget Lab at Yale: State of U.S. Tariffs, August 7, 2025 -- 18.6%, highest since 1933; 2.4% at the start of 2025; ~28% implied in April 2025

The Budget Lab at Yale: Tariff Rate Tracker -- open-source daily effective tariff rates from official HTS data

NPR: How companies avoid tariffs, from exemptions to engineering (March 7, 2025) -- Converse felt soles; Snuggie blanket ruling

CNBC: Tariff engineering is making a comeback (June 18, 2025) -- Columbia Sportswear pocket placement, 26.9% to 16%

Miller & Chevalier: Using the first sale rule to reduce tariffs

GAO-20-182: CBP risk management for tariff refunds should be improved -- ~$1 billion a year in drawback refunds

Federal Reserve Bank of New York, Liberty Street Economics: Who is paying for the 2025 U.S. tariffs? (February 2026) -- ~90% of burden on U.S. firms and consumers; relationship-level pass-through 65-70%; bargaining power lowers it

DLA Piper: DOJ launches Trade Fraud Task Force (September 2025)

Holland & Knight: Significant enforcement risks for tariff evasion (July 2025) -- 1,400 CBP penalties in H1 2025

DLA Piper: False Claims Act year in review 2025 (February 2026) -- record $6.8B recoveries; 1,297 qui tam suits

Customs & International Trade Law Blog: The $549.5M Perfectus settlement (May 22, 2026)

Mayer Brown: DOJ continues to use the False Claims Act for customs violations (January 2026) -- transshipment-through-Taiwan settlement

Frequently Asked Questions

What is tariff engineering, and is it legal?

Tariff engineering is designing or modifying a product so it genuinely qualifies for a lower-duty tariff classification -- like Converse adding felt to outsoles or Columbia placing pockets below the waistline. It is legal when the change is real, in place before importation, and honestly declared. Courts have upheld the practice for over a century; what is never legal is misdescribing what the product actually is.

What is the difference between tariff engineering and customs fraud?

Engineering changes the physical product or the real supply chain; fraud changes only the paperwork. Misclassifying goods, undervaluing invoices, or routing Chinese products through a third country with relabeled origin are False Claims Act territory -- and enforcement is at record levels, with a DOJ Trade Fraud Task Force, a $549.5 million settlement in May 2026, and historic whistleblower activity.

What is duty drawback and how much can be recovered?

Drawback refunds up to 99% of duties, taxes, and fees on imported goods that are subsequently exported or destroyed, including substitution matching at the tariff-code level. CBP pays out roughly $1 billion a year, and industry estimates suggest several times that goes unclaimed by eligible importers. Recovery works best when export links and entry data are tagged at award rather than reconstructed later.

What is the first-sale rule in customs valuation?

In qualifying multi-tier transactions, U.S. importers may declare customs value based on the first sale -- the manufacturer's price to the intermediary -- rather than the marked-up price the importer pays. It requires a bona fide arm's-length first sale with goods destined for the U.S. from the start, plus rigorous documentation, which is why adoption is low despite meaningful savings on high-duty goods.

Should suppliers or buyers absorb tariff costs?

New York Fed research on the 2025 tariffs found roughly 90% of the burden fell on U.S. firms and consumers overall -- but in established trading relationships pass-through was 65-70%, and large buyers with bargaining power paid less. In practice the split is negotiated: buyers who re-quote exposed parts and write tariff clauses with baselines, caps, sunsets, and reopeners consistently pay below the sticker rate.

What does a duty-loaded should-cost model look like?

It carries duty as an explicit line per part -- HTS code, country of origin, customs value -- alongside material, labor, overhead, and freight, and it updates when rates change rather than at budget season. That visibility is what makes the mitigation moves actionable: you cannot re-quote, re-classify, or reclaim what you cannot see at the part level.

Follow one number through the last eighteen months. The average effective U.S. tariff rate started 2025 at 2.4%. The announcements of April 2025 briefly implied a rate near 28%. By August the dust had settled at 18.6% -- the highest level since 1933 -- and then the exemptions and deals began: 17.4% in September, 18.0% in October, 16.9% in January. By this April the rate stood at 11.0%, and The Budget Lab at Yale projects roughly 9.7% once the Section 122 tariffs expire in July and the pharmaceutical tariffs arrive in September.

Related: the feed-forward idea this playbook leans on is part of a bigger argument -- Closed-Loop Procurement.

That is four distinct trade regimes inside eighteen months, spanning exactly one annual budget cycle. If your landed-cost assumptions were set in January 2025 and reconciled in December, the number you planned against was wrong by a factor of seven at the peak, and wrong in both directions before the year closed.

Most of what procurement people read about tariffs is written by trade lawyers and freight forwarders, and it shows: the advice is about entry filings and shipping lanes. This post is the buyer's version. Duty is now a cost element that moves faster than most commodity indices, and the levers that actually manage it -- classification, origin, valuation, recovery, negotiation -- are sourcing levers. They belong to whoever owns the bill of materials.

The number that would not sit still

It is worth sitting with the volatility for a moment, because it changes what kind of problem this is.

A stable tariff regime is a compliance problem: classify correctly, file correctly, audit occasionally. The 2025-2026 regime is a sourcing problem. When the rate on a Chinese subassembly can triple between quote and first shipment, and then fall by a third before the tooling amortizes, tariff exposure behaves like a volatile commodity input -- except that, unlike copper or resin, it moves on signatures rather than supply and demand, which means it gaps overnight and ignores your hedges.

Point readings from The Budget Lab's dated reports, connected for readability; the dashed segment is their April 2026 projection.

The buyers I watch getting through this are not the ones forecasting rates better. Nobody forecasts this well -- the Budget Lab's own reports read like weather bulletins. The buyers doing fine are the ones whose cost models absorb a rate change the way a good ERP absorbs a price change: as a data update, not a crisis meeting.

Duty is a BOM line, not a freight surcharge

Here is the structural problem with how most companies account for tariffs: they land in a freight or landed-cost bucket, blended across a category, visible only in aggregate. A surcharge arrives after every decision is frozen -- the part designed, the supplier quoted, the origin set, the contract signed. By the time duty shows up as a number anyone reviews, the choices that created it are months old.

A BOM line is different. It sits where the choices still exist.

The single highest-value change a procurement team can make on tariffs is accounting hygiene: carry duty as its own line on every exposed part -- HTS code times country of origin times customs value. A die casting from Vietnam, a wire harness from Mexico, and a machined bracket from China can sit in the same assembly with entirely different duty exposure and entirely different escape routes. Blend them and you can see that margin moved; you cannot see why, or what to do about it. Line them out and duty becomes what every other BOM element already is: should-costable, quotable, negotiable, and trackable against alternatives. It is the difference between knowing your total landed cost as a fact and knowing it as an average.

It also becomes forecastable, which matters more than usual right now. Announced-but-not-yet-effective changes are free information: the July expirations and September pharmaceutical tariffs are published, not speculative. A control engineer would call pricing them in before they hit feed-forward; a buyer should just call it Tuesday. Quote exposed parts three ways -- at award-date rates, at start-of-production rates, and at announced future rates -- and let finance reserve against the gap while sourcing works the mitigation list.

One clarification on ownership, because this is where the org chart usually fumbles the handoff. Trade compliance owns the legal entry, and nothing here changes that. But by the time an entry exists, most of the decisions that created the exposure -- supplier, location, value chain, contract terms -- were made at a sourcing desk, usually months earlier. Duty math has to live where those choices are made, with compliance as the control authority, not the discovery mechanism.

Move 1: Classify -- and engineer

Start with the unglamorous step: confirm that every exposed part's HTS code is actually correct. The Harmonized Tariff Schedule runs to ninety-nine chapters and the classification logic is genuinely tricky at the margins; misclassification cuts both ways, and overpaying is just as common as underpaying. On a BOM of any size, a classification audit of the top duty-paying lines is the fastest money in this post.

Then look for engineering options, because classification follows the physical product as imported -- and companies have been legally designing their way into better headings for over a century. The classics are worth knowing because they calibrate what counts as real:

Converse ships All Stars with a thin layer of felt on the outsole. Footwear with felt-covered soles classifies differently than athletic shoes, at a fraction of the duty. The felt wears off in weeks; classification is assessed at the moment of import, so the duty savings do not.

Columbia Sportswear adds small pockets below the waistline on certain women's shirts, moving them out of a 26.9% blouse classification into a 16% category. A designer, a customs broker, and a margin target, all in one garment.

The Snuggie's maker went to court over whether a fleece robe with sleeves is a garment or a blanket, and in 2017 the Court of International Trade ruled it a blanket -- 8.5% duty instead of 14.9%.

The pattern in all three: a real, physical, pre-importation product attribute, honestly declared, that genuinely changes what the thing is under the tariff schedule. For a manufacturer, the equivalent conversations are about material substitutions, where a subassembly gets joined, and what state of completion a part ships in. Those are engineering change orders with duty consequences -- run them through the same should-cost discipline as any other design-to-cost decision, and get a binding ruling from CBP when the classification is aggressive. A ruling letter is cheap; the alternative section of this post is not.

Move 2: Origin

Duty follows where the last substantial transformation happened, not where the purchase order went or where the supplier's headquarters sits. That makes origin a designable property of your supply chain -- within real limits.

Substantial transformation means the product genuinely became a different article of commerce somewhere: new name, new character, new use. Moving final processing steps, qualifying parts under USMCA content rules, and documenting the transformation properly are sourcing decisions a buyer controls, and in a high-tariff regime they deserve the same rigor as a make-versus-buy or dual-sourcing analysis. The China-plus-one conversations most manufacturers have been having for years are, among other things, origin-engineering conversations -- and the same compliance care applies to them as to China's own tightening export rules.

The caution is structural: paper routing is not origin engineering. A Chinese part that takes a boat detour through a third country and picks up a new label is still Chinese under the law, no matter what the certificate says. More on what happens to that move below.

Move 3: Value

Duty is a percentage of customs value, which makes the valuation basis the quietest lever on this list. The first-sale rule lets qualifying importers declare value based on the first sale in a multi-tier transaction -- the manufacturer's price to the trading company or intermediary -- rather than the marked-up price the importer actually pays.

On a part with a 25% duty and a 15% intermediary markup, first-sale valuation claws back nearly four points of landed cost without changing the product, the supplier, or the logistics. The requirements are strict: a bona fide arm's-length first sale, goods clearly destined for the United States at the time of that sale, and documentation that proves both -- purchase orders, invoices, payment records, and any assists accounted for. That paperwork burden is exactly why adoption stays low, and why the importers who build the documentation muscle keep the savings year after year. It is a classic cost-avoidance program: invisible in a savings report, very visible in landed cost.

Move 4: Recover

Money already paid is not necessarily money gone. Duty drawback refunds up to 99% of duties, taxes, and fees on imported goods that are subsequently exported or destroyed -- including substitution drawback, which matches imports and exports at the HTS level rather than requiring you to trace the physical molecules. Import components, build product, export some of it, and a meaningful slice of your duty bill is refundable.

The scale of the unclaimed pool is striking. CBP pays out roughly $1 billion a year in drawback, per the Government Accountability Office -- and industry estimates put the eligible refunds left unclaimed at several times that, mostly because the documentation feels daunting and nobody owns the program. The mechanics deserve their own post, and they have one: our practical guide to duty drawback walks through eligibility, filing, and the records you need. The strategic point belongs here: drawback fails when it is treated as an accounting cleanup. If export links, serial numbers, and entry data are not tagged at award time, the refund becomes archaeology. Design recovery into the sourcing data from day one.

Foreign-trade zones round out the recovery lane: duty deferral until goods leave the zone, no duty at all on re-exports, and -- in inverted-tariff cases where components carry higher rates than finished goods -- a structural rate reduction for manufacturing inside the zone.

Move 5: Renegotiate

Now the move most buyers reach for first, armed with the data to do it properly.

The New York Fed's analysis of who actually paid the 2025 tariffs found that about 90% of the burden landed on U.S. firms and consumers -- foreign exporters did not, in aggregate, eat much of it. But the average hides the finding that matters for a buyer: at the level of established importer-exporter relationships, pass-through ran 65-70%, and large buyers with bargaining power paid measurably less than small ones. Who absorbs the duty is a negotiation, not a law of nature, and passivity means paying the sticker rate.

Bargaining power is not personality. It is qualified alternatives, clean cost models, and credible volume movement -- the same assets that win any negotiation, pointed at a new cost element. Re-quote the exposed BOM lines specifically rather than asking for blanket relief; a supplier who sees you know exactly which parts carry which duty at which origin negotiates differently than one fielding a vague request to share the pain. Watch for price variance that quietly exceeds the actual statutory change -- tariff noise is a popular place to hide margin expansion, in both directions.

Then write the clause properly, because the 2025-2026 whipsaw taught everyone that rates fall too. A complete tariff clause defines the baseline HTS code and origin, the duty rate at signing, the valuation method, proof requirements, the sharing mechanism, a cap, a sunset, and a reopener -- so that when the rate drops, the price comes down by the same logic that raised it. Buyers who wrote one-directional clauses in 2025 are re-learning this now, on the wrong side of an 18.6%-to-11% move.

Smaller importers without volume to wield can still run most of this play: isolate the exposed lines, aggregate demand across plants and business units, prequalify a second source at a different origin as negotiating infrastructure, and refuse blended price increases that bundle duty with everything else.

The line between engineering and evasion

Everything above is legal, established, and in several cases blessed by federal courts. Its mirror image is a federal felony, and 2026 is the wrong year to confuse them.

The enforcement climate is the harshest in decades. The Justice Department stood up a dedicated Trade Fraud Task Force in August 2025, pairing DOJ attorneys with CBP's Office of Trade and Homeland Security Investigations. CBP issued 1,400 trade-enforcement penalties in the first half of 2025, on pace to beat every year in recent memory. False Claims Act recoveries hit an all-time record of $6.8 billion in fiscal 2025, with 1,297 whistleblower suits filed -- also a record. And four weeks ago, the task force announced the largest customs-fraud settlement in U.S. history: $549.5 million against an importer that evaded antidumping duties on Chinese aluminum. Another recent settlement involved Chinese tungsten carbide routed through Taiwan with relabeled origin paperwork.

The distinction between the playbook and the docket is not subtle. Felt on a sole is a real product, honestly declared, classified accordingly: engineering. A Taiwanese label on a Chinese part is paperwork pretending to be a supply chain: fraud. What has changed is the detection. CBP now runs AI-driven supply-chain analytics against import patterns to flag transshipment and undervaluation, and the False Claims Act pays whistleblowers a share of recoveries -- and the people best positioned to blow the whistle are your own employees, your competitors, and your suppliers.

The operating standard that follows: make the file readable by someone hostile. Every change in classification, origin, valuation, or recovery treatment should show what physically changed, who approved it, what documents support it, and which counsel or broker reviewed it. Binding rulings, origin documentation, first-sale paper trails -- the compliance file is not overhead on the playbook. It is the playbook's license to operate.

Where the desk work goes next

The reason most teams have not done what this post describes is not that any single move is hard. It is that the data work underneath -- duty at the BOM line, per part, per origin, refreshed as rates move, wired into quoting -- has historically been brutal to maintain by hand in spreadsheets. That is changing. Our customers at LightSource -- mostly challenger manufacturers running fast NPI cycles -- track tariff exposure at the BOM line, run what-if scenarios when an origin shift or rate change is announced, and re-quote the exposed parts in hours rather than quarters. The duty column updates the way the rest of their cost model does: continuously, not at budget season.

The rate will move again -- July's expirations, September's pharmaceutical tariffs, an election cycle behind those. The lesson of the last eighteen months is not which direction comes next; it is that nobody reliably knows, and the annual cost-down ritual was never built for a cost element that gaps overnight on a signature. The buyers getting through this are not forecasting better. They carry duty math in the BOM, they have rehearsed five legal moves, and when the schedule changes, they re-quote a column instead of convening a task force.

Sources

The Budget Lab at Yale: State of U.S. Tariffs, April 8, 2026 -- effective rate 11.0%; projections after July expirations and September pharmaceutical tariffs

The Budget Lab at Yale: State of U.S. Tariffs, August 7, 2025 -- 18.6%, highest since 1933; 2.4% at the start of 2025; ~28% implied in April 2025

The Budget Lab at Yale: Tariff Rate Tracker -- open-source daily effective tariff rates from official HTS data

NPR: How companies avoid tariffs, from exemptions to engineering (March 7, 2025) -- Converse felt soles; Snuggie blanket ruling

CNBC: Tariff engineering is making a comeback (June 18, 2025) -- Columbia Sportswear pocket placement, 26.9% to 16%

Miller & Chevalier: Using the first sale rule to reduce tariffs

GAO-20-182: CBP risk management for tariff refunds should be improved -- ~$1 billion a year in drawback refunds

Federal Reserve Bank of New York, Liberty Street Economics: Who is paying for the 2025 U.S. tariffs? (February 2026) -- ~90% of burden on U.S. firms and consumers; relationship-level pass-through 65-70%; bargaining power lowers it

DLA Piper: DOJ launches Trade Fraud Task Force (September 2025)

Holland & Knight: Significant enforcement risks for tariff evasion (July 2025) -- 1,400 CBP penalties in H1 2025

DLA Piper: False Claims Act year in review 2025 (February 2026) -- record $6.8B recoveries; 1,297 qui tam suits

Customs & International Trade Law Blog: The $549.5M Perfectus settlement (May 22, 2026)

Mayer Brown: DOJ continues to use the False Claims Act for customs violations (January 2026) -- transshipment-through-Taiwan settlement

Frequently Asked Questions

What is tariff engineering, and is it legal?

Tariff engineering is designing or modifying a product so it genuinely qualifies for a lower-duty tariff classification -- like Converse adding felt to outsoles or Columbia placing pockets below the waistline. It is legal when the change is real, in place before importation, and honestly declared. Courts have upheld the practice for over a century; what is never legal is misdescribing what the product actually is.

What is the difference between tariff engineering and customs fraud?

Engineering changes the physical product or the real supply chain; fraud changes only the paperwork. Misclassifying goods, undervaluing invoices, or routing Chinese products through a third country with relabeled origin are False Claims Act territory -- and enforcement is at record levels, with a DOJ Trade Fraud Task Force, a $549.5 million settlement in May 2026, and historic whistleblower activity.

What is duty drawback and how much can be recovered?

Drawback refunds up to 99% of duties, taxes, and fees on imported goods that are subsequently exported or destroyed, including substitution matching at the tariff-code level. CBP pays out roughly $1 billion a year, and industry estimates suggest several times that goes unclaimed by eligible importers. Recovery works best when export links and entry data are tagged at award rather than reconstructed later.

What is the first-sale rule in customs valuation?

In qualifying multi-tier transactions, U.S. importers may declare customs value based on the first sale -- the manufacturer's price to the intermediary -- rather than the marked-up price the importer pays. It requires a bona fide arm's-length first sale with goods destined for the U.S. from the start, plus rigorous documentation, which is why adoption is low despite meaningful savings on high-duty goods.

Should suppliers or buyers absorb tariff costs?

New York Fed research on the 2025 tariffs found roughly 90% of the burden fell on U.S. firms and consumers overall -- but in established trading relationships pass-through was 65-70%, and large buyers with bargaining power paid less. In practice the split is negotiated: buyers who re-quote exposed parts and write tariff clauses with baselines, caps, sunsets, and reopeners consistently pay below the sticker rate.

What does a duty-loaded should-cost model look like?

It carries duty as an explicit line per part -- HTS code, country of origin, customs value -- alongside material, labor, overhead, and freight, and it updates when rates change rather than at budget season. That visibility is what makes the mitigation moves actionable: you cannot re-quote, re-classify, or reclaim what you cannot see at the part level.

Follow one number through the last eighteen months. The average effective U.S. tariff rate started 2025 at 2.4%. The announcements of April 2025 briefly implied a rate near 28%. By August the dust had settled at 18.6% -- the highest level since 1933 -- and then the exemptions and deals began: 17.4% in September, 18.0% in October, 16.9% in January. By this April the rate stood at 11.0%, and The Budget Lab at Yale projects roughly 9.7% once the Section 122 tariffs expire in July and the pharmaceutical tariffs arrive in September.

Related: the feed-forward idea this playbook leans on is part of a bigger argument -- Closed-Loop Procurement.

That is four distinct trade regimes inside eighteen months, spanning exactly one annual budget cycle. If your landed-cost assumptions were set in January 2025 and reconciled in December, the number you planned against was wrong by a factor of seven at the peak, and wrong in both directions before the year closed.

Most of what procurement people read about tariffs is written by trade lawyers and freight forwarders, and it shows: the advice is about entry filings and shipping lanes. This post is the buyer's version. Duty is now a cost element that moves faster than most commodity indices, and the levers that actually manage it -- classification, origin, valuation, recovery, negotiation -- are sourcing levers. They belong to whoever owns the bill of materials.

The number that would not sit still

It is worth sitting with the volatility for a moment, because it changes what kind of problem this is.

A stable tariff regime is a compliance problem: classify correctly, file correctly, audit occasionally. The 2025-2026 regime is a sourcing problem. When the rate on a Chinese subassembly can triple between quote and first shipment, and then fall by a third before the tooling amortizes, tariff exposure behaves like a volatile commodity input -- except that, unlike copper or resin, it moves on signatures rather than supply and demand, which means it gaps overnight and ignores your hedges.

Point readings from The Budget Lab's dated reports, connected for readability; the dashed segment is their April 2026 projection.

The buyers I watch getting through this are not the ones forecasting rates better. Nobody forecasts this well -- the Budget Lab's own reports read like weather bulletins. The buyers doing fine are the ones whose cost models absorb a rate change the way a good ERP absorbs a price change: as a data update, not a crisis meeting.

Duty is a BOM line, not a freight surcharge

Here is the structural problem with how most companies account for tariffs: they land in a freight or landed-cost bucket, blended across a category, visible only in aggregate. A surcharge arrives after every decision is frozen -- the part designed, the supplier quoted, the origin set, the contract signed. By the time duty shows up as a number anyone reviews, the choices that created it are months old.

A BOM line is different. It sits where the choices still exist.

The single highest-value change a procurement team can make on tariffs is accounting hygiene: carry duty as its own line on every exposed part -- HTS code times country of origin times customs value. A die casting from Vietnam, a wire harness from Mexico, and a machined bracket from China can sit in the same assembly with entirely different duty exposure and entirely different escape routes. Blend them and you can see that margin moved; you cannot see why, or what to do about it. Line them out and duty becomes what every other BOM element already is: should-costable, quotable, negotiable, and trackable against alternatives. It is the difference between knowing your total landed cost as a fact and knowing it as an average.

It also becomes forecastable, which matters more than usual right now. Announced-but-not-yet-effective changes are free information: the July expirations and September pharmaceutical tariffs are published, not speculative. A control engineer would call pricing them in before they hit feed-forward; a buyer should just call it Tuesday. Quote exposed parts three ways -- at award-date rates, at start-of-production rates, and at announced future rates -- and let finance reserve against the gap while sourcing works the mitigation list.

One clarification on ownership, because this is where the org chart usually fumbles the handoff. Trade compliance owns the legal entry, and nothing here changes that. But by the time an entry exists, most of the decisions that created the exposure -- supplier, location, value chain, contract terms -- were made at a sourcing desk, usually months earlier. Duty math has to live where those choices are made, with compliance as the control authority, not the discovery mechanism.

Move 1: Classify -- and engineer

Start with the unglamorous step: confirm that every exposed part's HTS code is actually correct. The Harmonized Tariff Schedule runs to ninety-nine chapters and the classification logic is genuinely tricky at the margins; misclassification cuts both ways, and overpaying is just as common as underpaying. On a BOM of any size, a classification audit of the top duty-paying lines is the fastest money in this post.

Then look for engineering options, because classification follows the physical product as imported -- and companies have been legally designing their way into better headings for over a century. The classics are worth knowing because they calibrate what counts as real:

Converse ships All Stars with a thin layer of felt on the outsole. Footwear with felt-covered soles classifies differently than athletic shoes, at a fraction of the duty. The felt wears off in weeks; classification is assessed at the moment of import, so the duty savings do not.

Columbia Sportswear adds small pockets below the waistline on certain women's shirts, moving them out of a 26.9% blouse classification into a 16% category. A designer, a customs broker, and a margin target, all in one garment.

The Snuggie's maker went to court over whether a fleece robe with sleeves is a garment or a blanket, and in 2017 the Court of International Trade ruled it a blanket -- 8.5% duty instead of 14.9%.

The pattern in all three: a real, physical, pre-importation product attribute, honestly declared, that genuinely changes what the thing is under the tariff schedule. For a manufacturer, the equivalent conversations are about material substitutions, where a subassembly gets joined, and what state of completion a part ships in. Those are engineering change orders with duty consequences -- run them through the same should-cost discipline as any other design-to-cost decision, and get a binding ruling from CBP when the classification is aggressive. A ruling letter is cheap; the alternative section of this post is not.

Move 2: Origin

Duty follows where the last substantial transformation happened, not where the purchase order went or where the supplier's headquarters sits. That makes origin a designable property of your supply chain -- within real limits.

Substantial transformation means the product genuinely became a different article of commerce somewhere: new name, new character, new use. Moving final processing steps, qualifying parts under USMCA content rules, and documenting the transformation properly are sourcing decisions a buyer controls, and in a high-tariff regime they deserve the same rigor as a make-versus-buy or dual-sourcing analysis. The China-plus-one conversations most manufacturers have been having for years are, among other things, origin-engineering conversations -- and the same compliance care applies to them as to China's own tightening export rules.

The caution is structural: paper routing is not origin engineering. A Chinese part that takes a boat detour through a third country and picks up a new label is still Chinese under the law, no matter what the certificate says. More on what happens to that move below.

Move 3: Value

Duty is a percentage of customs value, which makes the valuation basis the quietest lever on this list. The first-sale rule lets qualifying importers declare value based on the first sale in a multi-tier transaction -- the manufacturer's price to the trading company or intermediary -- rather than the marked-up price the importer actually pays.

On a part with a 25% duty and a 15% intermediary markup, first-sale valuation claws back nearly four points of landed cost without changing the product, the supplier, or the logistics. The requirements are strict: a bona fide arm's-length first sale, goods clearly destined for the United States at the time of that sale, and documentation that proves both -- purchase orders, invoices, payment records, and any assists accounted for. That paperwork burden is exactly why adoption stays low, and why the importers who build the documentation muscle keep the savings year after year. It is a classic cost-avoidance program: invisible in a savings report, very visible in landed cost.

Move 4: Recover

Money already paid is not necessarily money gone. Duty drawback refunds up to 99% of duties, taxes, and fees on imported goods that are subsequently exported or destroyed -- including substitution drawback, which matches imports and exports at the HTS level rather than requiring you to trace the physical molecules. Import components, build product, export some of it, and a meaningful slice of your duty bill is refundable.

The scale of the unclaimed pool is striking. CBP pays out roughly $1 billion a year in drawback, per the Government Accountability Office -- and industry estimates put the eligible refunds left unclaimed at several times that, mostly because the documentation feels daunting and nobody owns the program. The mechanics deserve their own post, and they have one: our practical guide to duty drawback walks through eligibility, filing, and the records you need. The strategic point belongs here: drawback fails when it is treated as an accounting cleanup. If export links, serial numbers, and entry data are not tagged at award time, the refund becomes archaeology. Design recovery into the sourcing data from day one.

Foreign-trade zones round out the recovery lane: duty deferral until goods leave the zone, no duty at all on re-exports, and -- in inverted-tariff cases where components carry higher rates than finished goods -- a structural rate reduction for manufacturing inside the zone.

Move 5: Renegotiate

Now the move most buyers reach for first, armed with the data to do it properly.

The New York Fed's analysis of who actually paid the 2025 tariffs found that about 90% of the burden landed on U.S. firms and consumers -- foreign exporters did not, in aggregate, eat much of it. But the average hides the finding that matters for a buyer: at the level of established importer-exporter relationships, pass-through ran 65-70%, and large buyers with bargaining power paid measurably less than small ones. Who absorbs the duty is a negotiation, not a law of nature, and passivity means paying the sticker rate.

Bargaining power is not personality. It is qualified alternatives, clean cost models, and credible volume movement -- the same assets that win any negotiation, pointed at a new cost element. Re-quote the exposed BOM lines specifically rather than asking for blanket relief; a supplier who sees you know exactly which parts carry which duty at which origin negotiates differently than one fielding a vague request to share the pain. Watch for price variance that quietly exceeds the actual statutory change -- tariff noise is a popular place to hide margin expansion, in both directions.

Then write the clause properly, because the 2025-2026 whipsaw taught everyone that rates fall too. A complete tariff clause defines the baseline HTS code and origin, the duty rate at signing, the valuation method, proof requirements, the sharing mechanism, a cap, a sunset, and a reopener -- so that when the rate drops, the price comes down by the same logic that raised it. Buyers who wrote one-directional clauses in 2025 are re-learning this now, on the wrong side of an 18.6%-to-11% move.

Smaller importers without volume to wield can still run most of this play: isolate the exposed lines, aggregate demand across plants and business units, prequalify a second source at a different origin as negotiating infrastructure, and refuse blended price increases that bundle duty with everything else.

The line between engineering and evasion

Everything above is legal, established, and in several cases blessed by federal courts. Its mirror image is a federal felony, and 2026 is the wrong year to confuse them.

The enforcement climate is the harshest in decades. The Justice Department stood up a dedicated Trade Fraud Task Force in August 2025, pairing DOJ attorneys with CBP's Office of Trade and Homeland Security Investigations. CBP issued 1,400 trade-enforcement penalties in the first half of 2025, on pace to beat every year in recent memory. False Claims Act recoveries hit an all-time record of $6.8 billion in fiscal 2025, with 1,297 whistleblower suits filed -- also a record. And four weeks ago, the task force announced the largest customs-fraud settlement in U.S. history: $549.5 million against an importer that evaded antidumping duties on Chinese aluminum. Another recent settlement involved Chinese tungsten carbide routed through Taiwan with relabeled origin paperwork.

The distinction between the playbook and the docket is not subtle. Felt on a sole is a real product, honestly declared, classified accordingly: engineering. A Taiwanese label on a Chinese part is paperwork pretending to be a supply chain: fraud. What has changed is the detection. CBP now runs AI-driven supply-chain analytics against import patterns to flag transshipment and undervaluation, and the False Claims Act pays whistleblowers a share of recoveries -- and the people best positioned to blow the whistle are your own employees, your competitors, and your suppliers.

The operating standard that follows: make the file readable by someone hostile. Every change in classification, origin, valuation, or recovery treatment should show what physically changed, who approved it, what documents support it, and which counsel or broker reviewed it. Binding rulings, origin documentation, first-sale paper trails -- the compliance file is not overhead on the playbook. It is the playbook's license to operate.

Where the desk work goes next

The reason most teams have not done what this post describes is not that any single move is hard. It is that the data work underneath -- duty at the BOM line, per part, per origin, refreshed as rates move, wired into quoting -- has historically been brutal to maintain by hand in spreadsheets. That is changing. Our customers at LightSource -- mostly challenger manufacturers running fast NPI cycles -- track tariff exposure at the BOM line, run what-if scenarios when an origin shift or rate change is announced, and re-quote the exposed parts in hours rather than quarters. The duty column updates the way the rest of their cost model does: continuously, not at budget season.

The rate will move again -- July's expirations, September's pharmaceutical tariffs, an election cycle behind those. The lesson of the last eighteen months is not which direction comes next; it is that nobody reliably knows, and the annual cost-down ritual was never built for a cost element that gaps overnight on a signature. The buyers getting through this are not forecasting better. They carry duty math in the BOM, they have rehearsed five legal moves, and when the schedule changes, they re-quote a column instead of convening a task force.

Sources

The Budget Lab at Yale: State of U.S. Tariffs, April 8, 2026 -- effective rate 11.0%; projections after July expirations and September pharmaceutical tariffs

The Budget Lab at Yale: State of U.S. Tariffs, August 7, 2025 -- 18.6%, highest since 1933; 2.4% at the start of 2025; ~28% implied in April 2025

The Budget Lab at Yale: Tariff Rate Tracker -- open-source daily effective tariff rates from official HTS data

NPR: How companies avoid tariffs, from exemptions to engineering (March 7, 2025) -- Converse felt soles; Snuggie blanket ruling

CNBC: Tariff engineering is making a comeback (June 18, 2025) -- Columbia Sportswear pocket placement, 26.9% to 16%

Miller & Chevalier: Using the first sale rule to reduce tariffs

GAO-20-182: CBP risk management for tariff refunds should be improved -- ~$1 billion a year in drawback refunds

Federal Reserve Bank of New York, Liberty Street Economics: Who is paying for the 2025 U.S. tariffs? (February 2026) -- ~90% of burden on U.S. firms and consumers; relationship-level pass-through 65-70%; bargaining power lowers it

DLA Piper: DOJ launches Trade Fraud Task Force (September 2025)

Holland & Knight: Significant enforcement risks for tariff evasion (July 2025) -- 1,400 CBP penalties in H1 2025

DLA Piper: False Claims Act year in review 2025 (February 2026) -- record $6.8B recoveries; 1,297 qui tam suits

Customs & International Trade Law Blog: The $549.5M Perfectus settlement (May 22, 2026)

Mayer Brown: DOJ continues to use the False Claims Act for customs violations (January 2026) -- transshipment-through-Taiwan settlement

Frequently Asked Questions

What is tariff engineering, and is it legal?

Tariff engineering is designing or modifying a product so it genuinely qualifies for a lower-duty tariff classification -- like Converse adding felt to outsoles or Columbia placing pockets below the waistline. It is legal when the change is real, in place before importation, and honestly declared. Courts have upheld the practice for over a century; what is never legal is misdescribing what the product actually is.

What is the difference between tariff engineering and customs fraud?

Engineering changes the physical product or the real supply chain; fraud changes only the paperwork. Misclassifying goods, undervaluing invoices, or routing Chinese products through a third country with relabeled origin are False Claims Act territory -- and enforcement is at record levels, with a DOJ Trade Fraud Task Force, a $549.5 million settlement in May 2026, and historic whistleblower activity.

What is duty drawback and how much can be recovered?

Drawback refunds up to 99% of duties, taxes, and fees on imported goods that are subsequently exported or destroyed, including substitution matching at the tariff-code level. CBP pays out roughly $1 billion a year, and industry estimates suggest several times that goes unclaimed by eligible importers. Recovery works best when export links and entry data are tagged at award rather than reconstructed later.

What is the first-sale rule in customs valuation?

In qualifying multi-tier transactions, U.S. importers may declare customs value based on the first sale -- the manufacturer's price to the intermediary -- rather than the marked-up price the importer pays. It requires a bona fide arm's-length first sale with goods destined for the U.S. from the start, plus rigorous documentation, which is why adoption is low despite meaningful savings on high-duty goods.

Should suppliers or buyers absorb tariff costs?

New York Fed research on the 2025 tariffs found roughly 90% of the burden fell on U.S. firms and consumers overall -- but in established trading relationships pass-through was 65-70%, and large buyers with bargaining power paid less. In practice the split is negotiated: buyers who re-quote exposed parts and write tariff clauses with baselines, caps, sunsets, and reopeners consistently pay below the sticker rate.

What does a duty-loaded should-cost model look like?

It carries duty as an explicit line per part -- HTS code, country of origin, customs value -- alongside material, labor, overhead, and freight, and it updates when rates change rather than at budget season. That visibility is what makes the mitigation moves actionable: you cannot re-quote, re-classify, or reclaim what you cannot see at the part level.

Read more

Source Code Episode 9: Source Code: Shashi Mandapaty, Former Chief Procurement Officer at Johnson & Johnson, on Why One Throne Isn't Enough

Source Code Episode 8: Running on Paper: Rick McDonald, Chief Supply Chain Officer at Clorox, on Why Supplier Trust Is the Real Business Continuity Plan

The IEEPA Ruling Wasn't a Win. Here's What Procurement Leaders Are Missing.

Read more

Source Code Episode 9: Source Code: Shashi Mandapaty, Former Chief Procurement Officer at Johnson & Johnson, on Why One Throne Isn't Enough

Source Code Episode 8: Running on Paper: Rick McDonald, Chief Supply Chain Officer at Clorox, on Why Supplier Trust Is the Real Business Continuity Plan

The IEEPA Ruling Wasn't a Win. Here's What Procurement Leaders Are Missing.

Read more

Source Code Episode 9: Source Code: Shashi Mandapaty, Former Chief Procurement Officer at Johnson & Johnson, on Why One Throne Isn't Enough

Source Code Episode 8: Running on Paper: Rick McDonald, Chief Supply Chain Officer at Clorox, on Why Supplier Trust Is the Real Business Continuity Plan

The IEEPA Ruling Wasn't a Win. Here's What Procurement Leaders Are Missing.

Faster sourcing. Lower cost. Less chaos.

See how LightSource connects engineering, procurement, and suppliers in one operating system to help you launch faster at lower cost.

SOC 2

Kearney #1 2024

Gartner Cool Vendor

Procuretech 100

G2 Top Rated

Faster sourcing. Lower cost. Less chaos.

See how LightSource connects engineering, procurement, and suppliers in one operating system to help you launch faster at lower cost.

SOC 2

Kearney #1 2024

Gartner Cool Vendor

Procuretech 100

G2 Top Rated

Faster sourcing. Lower cost. Less chaos.

See how LightSource connects engineering, procurement, and suppliers in one operating system to help you launch faster at lower cost.

SOC 2

Kearney #1 2024

Gartner Cool Vendor

Procuretech 100

G2 Top Rated

Trusted by:

Trusted by:

Trusted by:

*GARTNER is a registered trademark and service mark of Gartner, Inc. and/or its affiliates in the U.S. and internationally, and COOL VENDORS is a registered trademark of Gartner, Inc. and/or its affiliates and are used herein with permission. All rights reserved. Gartner does not endorse any vendor, product or service depicted in its research publications, and does not advise technology users to select only those vendors with the highest ratings or other designation. Gartner research publications consist of the opinions of Gartner’s research organization and should not be construed as statements of fact. Gartner disclaims all warranties, expressed or implied, with respect to this research, including any warranties of merchantability or fitness for a particular purpose.